Are you struggling to find the right price for your product? Setting a price that covers your costs and brings in profit can feel like a tricky puzzle.

But what if you had a clear, simple way to price your product so you never leave money on the table? You’ll discover easy-to-follow steps that help you price your product for profit, attract more customers, and grow your business.

Keep reading, and you’ll learn how to turn your passion into a steady income with pricing strategies that really work for you.

Cost analysis is the first step in setting a profitable price for your product. It helps you understand all the expenses involved in making your product. Knowing these costs prevents losses and ensures you earn a fair profit. This section breaks down cost analysis into key parts to simplify the pricing process.

Direct costs are the expenses directly tied to making your product. These include raw materials and parts used in production. Calculate the total cost of these materials for one unit. Include any packaging costs that come with the product. These costs change with the number of items you produce.

Overhead expenses are indirect costs needed to run your business. They include rent, utilities, and equipment maintenance. Divide these costs over all products made to find the overhead cost per unit. Do not ignore these costs as they affect your total expenses. Overhead stays mostly fixed, no matter how many products you sell.

Labor costs cover the time workers spend on production. Calculate wages for each product based on hours worked. Include costs for materials that support production but are not part of the final product. Adding labor and materials to your direct and overhead costs gives a full picture. This total cost guides you in setting a price that covers expenses and earns profit.

Credit: www.shopify.com

Market research lays the foundation for setting the right price for your product. It helps you understand the market, your competition, and your customers. Good market research prevents pricing mistakes that can hurt your profit or sales. Use it to find a price that customers accept and that covers your costs with a profit margin.

Check prices of similar products in the market. Note the price range and what features affect pricing. Understand how competitors position their products. See if they offer discounts or bundles. This gives you a benchmark to set your price competitively. Avoid pricing too high or too low compared to others.

Know who will buy your product and what they value. Study their buying habits and spending power. Identify if they prefer low-cost or premium products. Consider their willingness to pay for extra features or quality. Tailor your price to meet their expectations and affordability.

Gauge how much demand exists for your product. Look at sales trends and customer interest. Higher demand can allow for a higher price. Low demand may require a lower price or added value. Use surveys or test sales to measure interest before final pricing.

Choosing the right pricing model shapes your product’s success. It affects sales volume, profits, and customer perception. Understanding different pricing models helps you set prices that fit your business goals.

Each pricing model offers a unique way to balance costs, value, and competition. Some focus on costs, others on customer value or market trends. Explore these common pricing models to find the best fit for your product.

Cost-plus pricing adds a fixed percentage to the product’s cost. This percentage is the profit margin. It ensures you cover expenses and earn a set profit. This method is simple and easy to calculate. It works well for products with stable costs and low market competition.

Value-based pricing sets prices based on customer perceived value. It focuses on how much customers are willing to pay. This model can increase profits if customers see high value. It requires understanding customer needs and benefits. It suits unique or premium products that solve specific problems.

Competitive pricing uses market prices as a guide. You set prices close to your competitors’ prices. This model keeps your product attractive in the market. It works well in industries with many similar products. Watch competitors’ prices regularly and adjust yours to stay relevant.

Dynamic pricing changes prices based on demand and supply. It uses data and algorithms to adjust prices in real-time. This model maximizes profit during high demand periods. It also helps clear inventory during low demand. Airlines and hotels often use dynamic pricing for better revenue.

Credit: business.bankofamerica.com

Profit margins show how much money you keep from each sale after covering costs. They help you understand if your product pricing is working well. Good profit margins mean your business can grow and pay bills easily.

Knowing your profit margins guides your pricing choices. Set prices too low, and profits shrink. Set prices too high, and customers may not buy. Finding the right balance is key to success.

Markup is the amount added to the cost price to get the selling price. It is usually a percentage of the cost. For example, if an item costs $10 and you want a 50% markup, you sell it for $15.

Decide on a markup based on your industry and competition. Higher markups increase profits but may reduce sales. Lower markups may attract customers but lower your profit per sale.

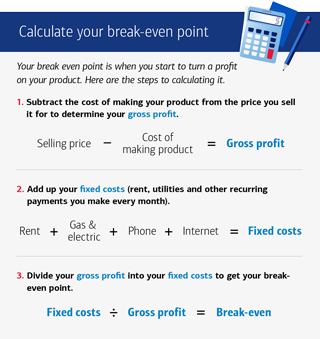

The break-even point shows how many units you must sell to cover all costs. It includes fixed costs like rent and variable costs like materials. Selling fewer than this number causes losses.

Use this formula: Break-Even Point = Fixed Costs ÷ (Price – Variable Cost). This helps you set realistic sales goals. Knowing your break-even point protects your business from losses.

Gross profit is the difference between sales revenue and the cost of goods sold. Increasing gross profit means earning more from each sale. You can do this by lowering costs or raising prices.

Control your costs by finding cheaper suppliers or reducing waste. Raise prices carefully by adding value or improving product quality. Both strategies help increase your overall profit margin.

Psychological pricing uses human behavior to set prices that attract buyers. It helps create a feeling of value or urgency. This approach can increase sales without lowering your profit margin. Understanding how customers think about prices is key to effective pricing.

Price anchoring sets a higher price first to make other prices seem better. Showing an expensive option next to a cheaper one makes the cheaper price look like a good deal. This helps customers feel they get more value for less money. Use anchoring to guide customers to your preferred price point.

Charm pricing ends prices with .99 or .95 to make them seem lower. For example, $9.99 feels cheaper than $10.00 even if the difference is small. This small change tricks the brain into thinking the price is less. Charm pricing encourages quick buying decisions.

Pricing tiers offer different product versions at various price points. Customers can choose based on their needs and budget. Tiers make your product feel flexible and accessible. They also help upsell by showing better value in higher tiers.

Credit: betterproposals.io

Adjusting prices is a key step in keeping your product profitable. Prices should change with the market and customer needs. Staying flexible helps you remain competitive and protect your profit margins. Learning when and how to adjust prices keeps your business strong.

Markets shift due to trends, competition, and costs. Watch these changes closely. If competitors lower prices, consider a small drop to stay attractive. If supply costs rise, a price increase may be needed. Reacting quickly helps keep your sales steady and profits healthy.

Discounts can boost sales but use them wisely. Offer discounts during slow periods or special events. Avoid frequent discounts to prevent customers from expecting lower prices all the time. Set clear goals for each discount to ensure it supports your profit, not hurts it.

Some customers care a lot about price, others less. Test different prices to see how sales change. Use surveys or sales data to find the best price point. Understanding price sensitivity helps you set prices that balance sales volume and profit.

Choosing the right tools can simplify pricing your product for profit. These resources help calculate costs, track profits, and analyze the market. Using the right tools saves time and increases accuracy in pricing decisions.

Pricing calculators help figure out the best price fast. Enter your costs, and they suggest a price that covers expenses and profit. Some calculators include tax and shipping costs. This tool prevents pricing too low or too high.

Profit margin trackers monitor how much money you make per sale. They show if your price covers costs and leaves room for profit. Trackers update with sales data, helping adjust prices over time. This tool keeps profits healthy and consistent.

Market analysis software studies competitors and customer trends. It shows popular price points and demand levels. This helps set a price that fits the market and attracts buyers. The software provides insights to stay competitive and profitable.

Calculate total costs, including production and overhead. Add a profit margin based on market demand. Set a competitive price that covers costs and ensures profit. Monitor sales and adjust pricing to maximize profitability.

The 5 C’s of pricing are Cost, Customers, Competition, Channel, and Compatibility. These factors guide effective pricing decisions.

The 7 C’s of pricing are Cost, Customers, Competition, Channel, Compatibility, Communication, and Consistency. They guide effective pricing strategies.

The 3 C’s of pricing cost are Cost, Customers, and Competition. They guide setting profitable, market-fit prices.

Pricing your product right takes careful thought and clear steps. Know your costs well before setting any price. Study your market to find what customers will pay. Add a fair profit margin that keeps your business growing. Test your price and adjust it based on sales feedback.

Keep prices simple and easy to understand. Good pricing helps your product succeed and your business thrive. Stay flexible and watch the market to stay profitable.

Leave A Reply Now